The global water clarifier industry has entered a phase of intense commercial activity since 2022, marked by a wave of product launches, strategic partnership formations, and mega-project contract awards that collectively redefine the competitive landscape. Veolia Water Technologies unveiled its next-generation Actiflo Turbo

high-rate clarifier at IFAT Munich 2024, integrating real-time turbidity feedback loops that optimize microsand injection and cut polymer use by up to 20 percent. SUEZ countered with an enhanced Densadeg lamella system featuring automated sludge

blanket sensors for phosphorus polishing at municipal plants upgrading to meet the EU’s recast Urban Waste Water Treatment Directive. Nordic Water Products, a Sulzer subsidiary, introduced a factory-assembled Meva tube settler module designed for containerized shipment to mining camps in Africa and South America, slashing on-site installation time to under four weeks. Strategic collaborations have multiplied, with ACCIONA and FCC Aqualia signing framework agreements with several Gulf Cooperation Council utilities to bundle clarifier packages into long-term design-build-operate contracts, and Larsen & Toubro partnering with Ion Exchange India to supply circular clarifiers for the Jal Jeevan Mission’s rural sewage treatment expansion.

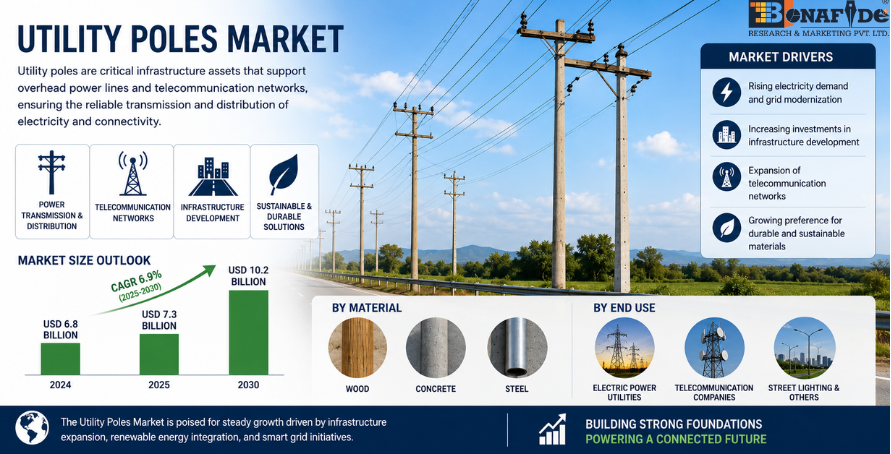

According to the research report "Global Water Clarifiers Market Outlook, 2031," published by Bonafide Research, the Global Water Clarifiers market was valued at more than USD 9.06 Billion in 2025, and expected to reach a market size of more than USD 13.13 Billion by 2031 with the CAGR of 6.55% from 2026-2031. On the M&A front, Xylem completed the integration of Evoqua Water Technologies, consolidating the Envirex clarifier range under its municipal solutions portfolio, while Metito acquired a controlling stake in a Turkish lamella plate fabricator to strengthen its Middle Eastern and North African supply chain. Contract activity surged as Saudi Arabia’s SWPC awarded the Al Haer ISTP concession, embedding large-diameter primary clarifiers, and Brazil’s SABESP commissioned multiple secondary clarifier retrofits under the Novo Marco do Saneamento. These developments reflect a structural shift: clarifier procurement is no longer a transactional equipment purchase but a bundled solution delivery that combines hydraulic design, chemical dosing,

digital monitoring, and multi-year O&M commitments into a single performance contract. Obstacles persist in the form of rising

stainless steel prices and the skilled workforce deficit documented by the American Water Works Association, yet the accelerated adoption of modular, digitally instrumented clarifiers across municipal and industrial water reuse schemes signals enduring momentum. Trade platforms like WEFTEC in Chicago and Singapore International Water Week have become launchpads for these innovations, while regional tax incentives India’s 12 percent GST on treatment equipment, Brazil’s REIDI sanitation incentive, and Saudi Arabia’s IKTVA local content requirements further shape the investment calculus for manufacturers and EPC consortia alike.

Installed pricing for a 35-metre conventional clarifier ranges from approximately $600,000 for a basic

carbon steel basin in a low-cost Asian market to over $2 million for a seismically engineered 316L stainless steel unit in Chile, with polymer dosing skids and

SCADA integration adding another 20 to 30 percent. Consumer behavior among public utility engineering departments exhibits deep institutional inertia; a plant manager in Lyon or Philadelphia will typically sole-source from the incumbent supplier that provided the original clarifiers, provided service responsiveness remains acceptable. Enterprise adoption by industrial operators PepsiCo in India, Nestl? in Brazil, and BHP in Chile is increasingly linked to corporate water stewardship pledges that demand clarifier pretreatment for reuse. Investment flows from the European Investment Bank’s water portfolio, the Asian Infrastructure Investment Bank’s sanitation lending, the World Bank’s municipal PPP programs, and the Saudi Water Partnership Company’s offtake-backed concessions, creating a durable global pipeline.

Municipal sewage plants deploy primary clarifiers to strip settleable solids and secondary clarifiers to separate activated sludge, both indispensable to the conventional treatment processes adopted by national design standards. Drinking water plants from Mexico City to Istanbul use clarifiers for floc sedimentation prior to filtration, managing turbidity spikes from seasonal runoff. Large-capacity installations dominate municipal procurement, with cities like Shanghai and Delhi ordering 50-metre-diameter circular units that handle peak flows for populations exceeding ten million. The most common design in public works is the concrete circular center-feed clarifier with a rotating half-bridge scraper and V-notch weirs, a configuration refined for operator simplicity. Municipal purchasing accounts for the overwhelming majority of clarifier unit volumes because thousands of publicly owned treatment works exist in the US alone, each operating multiple clarifiers. Standardization across state design manuals and national codes enables repetitive bidding, lowering engineering costs and attracting competitive fabrication. The institutional preference for proven, low-maintenance mechanics over complex internals sustains municipal leadership as the stable, enduring demand anchor.

California’s Title 22 reuse regulation demands effluent turbidity below 2 NTU, a standard secondary clarifiers alone cannot reliably meet, spurring tertiary lamella installations at facilities like the Orange County Groundwater Replenishment System. Singapore’s PUB requires all NEWater factories to operate high-rate solids-contact clarifiers ahead of reverse osmosis, protecting membranes and extending their operational life. Semiconductor fabs in Taiwan and South Korea integrate lamella settlers with polyaluminum chloride dosing to pretreat reclaim streams for ultrapure water production, critical to TSMC’s water positivity targets. Oil and gas operators in the Permian Basin and the Arabian Gulf deploy clarifiers for produced water polishing prior to enhanced oil recovery reinjection. Municipal aquifer recharge schemes in Windhoek and El Paso embed primary and secondary clarifiers as the initial solids-separation step before advanced oxidation. Clarifier performance expectations in reuse applications now routinely demand stable solids capture at

surface overflow rates of 2–4 meters per hour, independent of diurnal flow swings, driving adoption of automated desludging and polymer feedback systems.

Food and

beverage processors like PepsiCo and Nestl? have installed tube settler clarifiers to recover condensate and wash water, converting effluent from a disposal liability into a process asset and reinforcing reuse as the fastest-growing application segment.

The central feedwell dissipates inflow energy while promoting flocculation, and laminar outward flow toward peripheral weirs ensures uniform collection with minimal short-circuiting, a hydraulic profile validated by thousands of installations. Operating mechanisms rely on

motor-driven scraper bridges that continuously convey settled sludge to a bottom hopper, a straightforward system that plant operators maintain without specialized instrumentation skills. Space requirements are generous, yet most treatment plants built during the global infrastructure expansion of the 1970s through 1990s reserved ample land, making footprint a secondary concern for retrofit projects. Typical outdoor concrete basins in freeze thaw climates, from Ontario to Scandinavia, use heated weir covers and heavy-duty drives from DBS Manufacturing to ensure winter reliability. Capacity suitability for peak wet-

weather flows up to three times average dry-weather flow makes these clarifiers indispensable for combined sewer systems in cities like Brussels and Philadelphia. The design’s tolerance of bulking sludge during filamentous bacteria episodes offers a safety net that compact high-rate systems cannot replicate without plate blinding risks. Municipal engineering departments worldwide replicate proven geometries in successive capital improvement plans, creating a self-sustaining procurement loop that keeps conventional clarifiers at the top of the global type hierarchy.

Final phosphorus precipitation to below 0.3 mg/L at German Ruhrverband and Swiss ARA Bern plants relies on tube settlers that capture chemical flocs, simultaneously removing residual suspended solids that interfere with UV disinfection. Effluent quality improvement for direct aquifer recharge in California and Spanish Murcia requires tertiary lamella clarifiers to strip fine flocs escaping secondary treatment, protecting downstream reverse osmosis membranes from particulate fouling. Reuse-oriented installations at Singapore’s NEWater factories and Brisbane’s Western Corridor scheme use high-rate tertiary clarifiers to maintain TSS below 5 mg/L, meeting the stringent pretreatment requirements of dual-

membrane systems. Integration with ozonation and granular

activated carbon at Z?rich’s Werdh?lzli plant shows that clarified effluent improves ozone mass transfer efficiency, reducing disinfection byproduct formation. Conversion of decommissioned chlorine contact tanks into tertiary clarifier modules, as done at Thames Water’s Beckton facility, slashes capital costs by enabling reuse of existing civil infrastructure. Seasonal algae blooms in the Baltic Sea and Great Lakes force utilities to activate tertiary clarification specifically during summer, when secondary tanks are overwhelmed by buoyant flocs. Industrial pharmaceutical complexes near Basel and Hyderabad deploy tertiary clarifiers to consistently meet TSS consents below 10 mg/L, a target secondary units cannot guarantee during production campaign changes.

A city serving between 100,000 and 500,000 residents typically sizes its primary and secondary clarifiers within this capacity bracket, as exemplified by plants in Toulouse, France, and Surat, India, where multiple parallel units manage combined flows. Food processing complexes, including dairy operations run by Arla Foods and Fonterra, deploy clarifiers of this size to handle sanitation shift washdown peaks that briefly exceed normal throughput. Design flexibility within this range permits both circular and rectangular configurations, allowing engineers to tailor basin geometry to site constraints without resorting to costly high-rate compact systems. A broad cross-section of industries breweries,

pulp and paper mills, chemical parks operates in this flow band because it balances capital outlay with operational robustness, avoiding the extreme civil costs of gigascale installations. Standard drive units and scraper bridges from manufacturers like Nordic Water and WesTech are catalog items in this capacity segment, reducing lead times and simplifying aftermarket parts procurement. Application diversity within this band spans drinking water pre-sedimentation, primary sewage settling, and industrial effluent pretreatment, making it the most universally applicable sizing category. The sheer numeric count of treatment facilities worldwide operating clarifiers in the 1,000–2,000 m?/h range ensures this capacity segment commands the largest share of unit orders and service revenues.

We are friendly and approachable, give us a call.

We are friendly and approachable, give us a call.